Table of Contents

- Understanding the Three-Week Reality Check for Commercial Financing

- Types of Commercial Financing and Which Fit a Three-Week Timeline

- Commercial Loan Documentation Checklist: Audit-Ready Financials

- Fast Commercial Loan Approval Process: Step-by-Step Timeline

- Tips for Getting Business Loans Approved Quickly: Lender Communication Templates

- Alternative Commercial Financing Options for Rapid Capital Access

- Common Mistakes That Delay Commercial Financing Approval

- How to Secure Commercial Financing in Three Weeks: Action Checklist

Secure Commercial Financing in Three Weeks: A Strategic Guide

Last Updated: July 11, 2026

Getting access to capital quickly separates businesses that seize opportunities from those stuck in endless underwriting cycles. At Asset Point Capital, we’ve tracked hundreds of commercial financing deals, and the companies that close fastest share a common trait: they approach the process like a project manager, not a loan applicant.

This guide walks you through exactly how to structure your three-week financing push, which financing types fit this timeline, what documents lenders demand, and the communication strategies that keep deals moving when every day counts.

Understanding the Three-Week Reality Check for Commercial Financing

The three-week timeline is achievable, but only if you understand what’s happening behind the scenes. Lenders don’t move faster because you ask nicely, they move faster because you’ve eliminated friction from their process. When a lender can verify your information, assess your creditworthiness, and confirm your ability to service debt without chasing you for missing documents, underwriting accelerates naturally.

This timeline assumes your financial statements are audit-ready (organized and verifiable), your business credit profile is clean, and your tax returns are filed and accessible. If these don’t exist yet, three weeks becomes impossible. But if you’ve prepared, three weeks is entirely realistic.

Start gathering documents two weeks before you apply. Most delays happen because applicants submit incomplete packages and lenders spend days requesting missing items. Pre-assembled documentation cuts underwriting time in half.

The biggest mistake businesses make is treating the three-week timeline as passive. You can’t submit an application and disappear. Instead, actively manage the lender’s workflow: respond to requests within 24 hours, flag questions immediately, and provide information in the exact format the lender requests.

Types of Commercial Financing and Which Fit a Three-Week Timeline

Not all commercial financing moves at the same speed. Traditional bank loans take 45-60 days. SBA guaranteed loans stretch to 90+ days. But certain financing structures are built for speed.

Bridge loans close in 7-14 days because they rely on collateral value, not cash flow analysis. If you have real estate to pledge, bridge financing easily meets your three-week goal.

Hard money loans close in 3-5 days, with higher interest rates and more restrictive terms. If speed is your primary objective, hard money is worth evaluating.

Commercial lines of credit from established lenders close in two weeks if you already have a banking relationship. The lender already knows your business and understands your cash flow patterns.

Asset-based lending ties your loan amount to specific collateral, inventory, accounts receivable, or equipment. Because the lender’s risk is backed by tangible assets, they approve faster.

Traditional commercial loans from regional banks sometimes hit three weeks, depending on underwriting capacity and application complexity. Smaller regional banks often move faster than national chains.

Speed in commercial financing is directly correlated with collateral. The more tangible assets backing your loan, the faster lenders will move. If you lack collateral, expect the timeline to extend beyond three weeks.

Secured vs. Unsecured Loans: Speed and Collateral Trade-Offs

Secured loans close faster than unsecured loans. When a lender can seize specific assets if you default, their risk profile improves dramatically, enabling faster approval.

A secured loan backed by real estate, equipment, or inventory typically closes in 7-21 days. The lender’s underwriting focuses on asset valuation and your ability to service debt. Both can be verified quickly with documentation ready.

Unsecured loans rely entirely on creditworthiness and business cash flow, requiring deeper financial analysis. Most unsecured commercial loans take 30-45 days minimum.

For a three-week timeline, secured financing is your best bet. If you have real property, equipment, or inventory, use it as collateral. The speed gain justifies the risk profile change.

Commercial Loan Documentation Checklist: Audit-Ready Financials

This is where most businesses fail their three-week timeline. They submit incomplete or poorly organized documentation, lenders request clarifications, and two weeks evaporate.

Audit-ready doesn’t mean formal audits, it means your financial statements are organized, verifiable, and error-free. A lender should understand your financial position within 30 minutes of reviewing your balance sheet, income statement, and cash flow statement.

Before applying, organize your financial records. This single activity has the highest impact on accelerating approval.

Submitting disorganized financial statements is the fastest way to blow your three-week timeline. Lenders will request clarifications, demand corrections, and potentially reject your application. Spend one week organizing before you apply.

Essential Documents Needed for Financing

Personal tax returns (last 2 years) show your personal income and tax filing history.

Business tax returns (last 2 years) demonstrate actual profitability.

Bank statements (last 3-6 months) show your cash position and transaction patterns.

Balance sheet and income statement (current month and last 2 years) form the foundation of the lender’s credit decision.

Cash flow projections (12 months forward) demonstrate your ability to service debt.

Articles of incorporation or business formation documents prove legal establishment.

Personal and business credit reports require your authorization.

Proof of business license and insurance show legal operation.

Ownership documentation for any pledged collateral (deeds, titles, equipment lists with fair market values).

Organize these documents in a single folder before contacting lenders. When a lender requests something, provide it within 24 hours.

Preparing Audit-Ready Financial Statements

Balance sheet: Assets must equal liabilities plus equity. Reconcile account balances until everything ties out.

Income statement: Revenue, cost of goods sold, operating expenses, and net income should flow logically. Be prepared to explain significant changes.

Cash flow statement: Shows how cash moved through your business and reconciles net income to actual cash position.

Supporting schedules: Prepare detailed schedules for significant debt, accounts receivable, or inventory. Have explanations ready for major variances.

Reconciliations: Bank reconciliations and account reconciliations should be current.

The goal is to make a lender’s job easy. They should review your statements, ask clarifying questions, and move forward without discovering errors later.

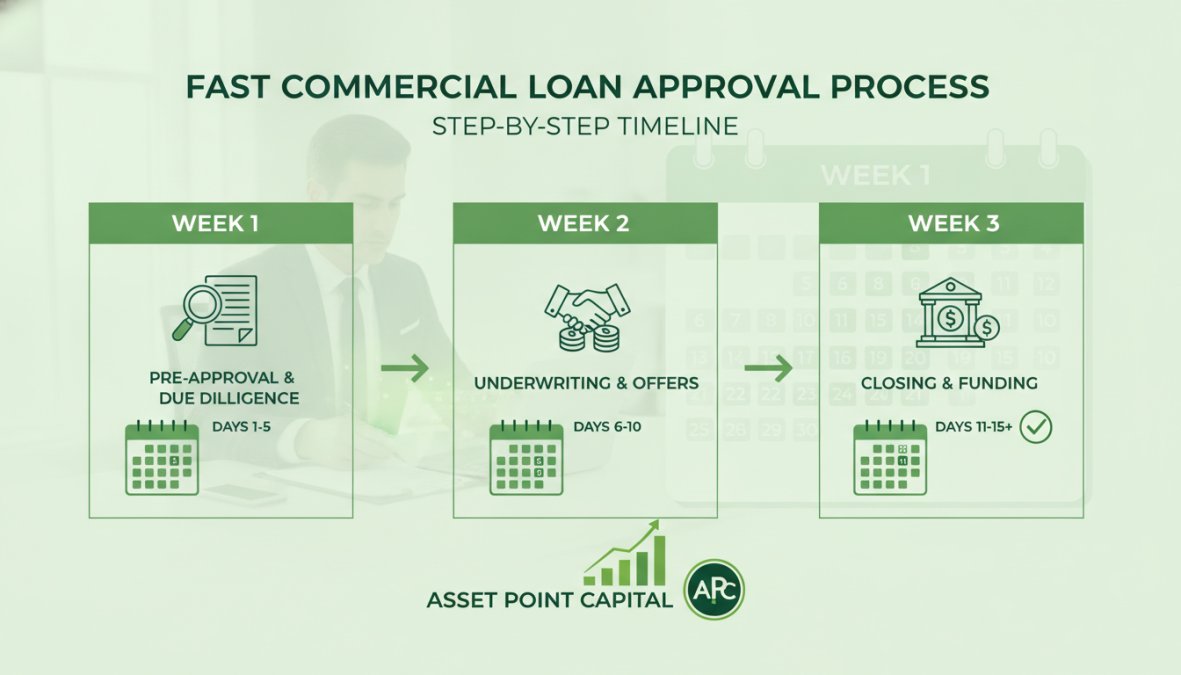

Fast Commercial Loan Approval Process: Step-by-Step Timeline

Three weeks breaks into three distinct phases: pre-qualification and submission, underwriting and verification, and approval and funding.

Week One: Pre-Qualification and Initial Submission

Days 1-2: Contact lenders and request pre-qualification. Describe your financing need, collateral position, and timeline. Lenders will tell you whether your deal fits their criteria and what documentation they’ll need.

Days 3-4: Prepare your complete documentation package using the checklist above. Don’t submit anything until you have 100% of requested documents.

Days 5-7: Submit your complete application with a cover letter explaining your financing need, qualifications, and timeline. Be direct about needing a decision within three weeks.

The goal of week one is to get your complete application in front of the lender with zero missing documents.

Week Two: Underwriting and Verification

Days 8-10: Lender reviews your application and requests clarifications. Respond within 24 hours.

Days 11-12: Lender verifies collateral through appraisals, ownership verification, or physical inspections. Coordinate quickly.

Days 13-14: Lender completes underwriting analysis of your credit, cash flow, collateral value, and debt service ability.

Week two is where most delays happen. Staying responsive is critical.

Week Three: Approval and Funding

Days 15-18: Lender issues conditional or final approval.

Days 19-21: Legal documents are prepared and executed. You sign the promissory note, security agreement, and loan documents.

Day 21: Funding transfers to your business account.

This timeline assumes you’re responsive, documentation is complete, and there are no major credit or collateral issues.

Tips for Getting Business Loans Approved Quickly: Lender Communication Templates

Lenders approve deals faster when they feel confident you’re organized and serious.

Building Your Lender Communication Strategy

Initial Inquiry Email:

Subject: Commercial Financing Request – [Your Business Name] – [Financing Amount]

Dear [Lender Name],

I’m seeking [financing amount] for [specific purpose]. Here’s a brief overview:

- Business type: [Industry and description]

- Annual revenue: [Amount]

- Collateral available: [Type and estimated value]

- Desired timeline: 3 weeks to closing

- Loan purpose: [Specific use]

I’ve attached a one-page summary. Are you available for a 15-minute call this week?

Best regards,

[Your name]

This email is direct, specific, and respects the lender’s time.

Complete Application Submission:

Subject: Commercial Financing Application – [Your Business Name] – Complete Documentation Package

Dear [Lender Name],

Per our conversation, I’m submitting our complete application for [amount].

Enclosed are:

- Personal tax returns (2024, 2025)

- Business tax returns (2024, 2025)

- Current financial statements

- 12-month cash flow projections

- Bank statements (last 6 months)

- Business license and insurance documentation

- Credit authorization forms

- [Additional documents specific to your deal]

All documents are current as of [date]. Our timeline is 3 weeks to closing. Please let me know what additional information you need.

Best regards,

[Your name]

Response to Lender Requests:

Subject: RE: Documentation Request – [Your Business Name]

Dear [Lender Name],

Thank you for your request regarding [specific item]. I’ve attached [document/explanation] as requested.

[Provide context that helps the lender understand the item.] I’m available by phone at [number] if you’d like to discuss any aspect of the application.

Best regards,

[Your name]

Lenders approve faster when applicants respond within 24 hours. Set up a dedicated email folder for your financing deal and check it multiple times daily.

Alternative Commercial Financing Options for Rapid Capital Access

If traditional commercial loans won’t meet your three-week timeline, consider alternatives.

Merchant cash advances provide capital within 7-10 days by advancing against future credit card sales. You repay through a percentage of daily transactions. The cost is higher, but the speed is unmatched.

Equipment financing closes in 2-3 weeks if you know exactly what equipment you’re purchasing. The equipment serves as collateral, so underwriting focuses on equipment value and your ability to pay.

Invoice factoring converts accounts receivable into immediate cash within 3-5 days. You repay when the customer pays the invoice. This works for B2B businesses with creditworthy customers.

Revolving lines of credit from online lenders fund in 5-7 days if approved. These are typically under $100,000 but sufficient for working capital needs.

Real estate investment loans from specialized lenders close in 2-3 weeks because they’ve simplified underwriting. If you’re financing a property acquisition or refinancing, a real estate specialist often beats traditional lenders on timeline.

Each alternative has trade-offs. Merchant cash advances cost more. Equipment financing requires knowing your equipment needs. Invoice factoring requires outstanding invoices. But if traditional loans won’t fit your timeline, these keep you moving forward.

Common Mistakes That Delay Commercial Financing Approval

Incomplete applications are the single biggest delay. Submit complete applications only.

Disorganized financial statements force lenders to ask clarifying questions. Spend time organizing before you apply.

Unresponsive applicants frustrate lenders. Respond within 24 hours, always.

Inflated financial projections create credibility problems. Be realistic in your projections.

Personal credit issues you haven’t disclosed. Disclose issues upfront and explain the context.

Collateral complications delay deals. Know your collateral position before you apply.

Changing your financing need mid-application creates rework. Nail down your financing need before you apply.

The common thread: preparation and responsiveness. Deals that close in three weeks are driven by applicants who’ve done their homework and stay engaged throughout the process.

How to Secure Commercial Financing in Three Weeks: Action Checklist

| Task | Timeline | Owner | Status |

|---|---|---|---|

| Organize financial records and reconcile accounts | Week -1 | You | – [ ] |

| Prepare audit-ready financial statements | Week -1 | You | – [ ] |

| Gather all required documentation | Week -1 | You | – [ ] |

| Research and identify target lenders | Days 1-2 | You | – [ ] |

| Submit pre-qualification inquiries | Days 3-4 | You | – [ ] |

| Prepare complete application package | Days 5-7 | You | – [ ] |

| Submit complete application | Day 7 | You | – [ ] |

| Respond to lender clarifications | Days 8-14 | You | – [ ] |

| Coordinate collateral verification | Days 11-14 | You | – [ ] |

| Receive conditional or final approval | Days 15-18 | Lender | – [ ] |

| Execute loan documents | Days 19-21 | You + Lender | – [ ] |

| Receive funding | Day 21 | Lender | – [ ] |

Print this checklist and track your progress daily.

Securing commercial financing quickly requires preparation, organization, and active management. Most businesses underestimate the work involved in weeks one and two, then panic when approval timelines slip. By preparing audit-ready financial statements, assembling complete documentation, and staying responsive to lender requests, three weeks is entirely achievable. Asset Point Capital specializes in closing real estate financing deals in 2-3 weeks by combining direct lending capability with access to over 1,025 niche market options. If you’re ready to move forward with commercial financing and need a lender who understands speed, Asset Point Capital provides firm term sheets within 24 hours and funds in as little as 2-3 weeks. Get started today and move from application to capital in the timeframe your business needs.

Frequently Asked Questions

Is it realistic to secure commercial financing in three weeks?

Yes, but only with proper preparation. Three weeks requires pre-qualified documentation, a clear capital need, and responsive lender communication. The timeline depends on loan type, secured commercial financing with strong collateral and complete financial statements moves faster than unsecured options. Lenders offering streamlined underwriting processes and firm term sheets within 24 hours can compress approval cycles significantly, making three weeks achievable for prepared borrowers.

What documents are needed for fast commercial loan approval?

Fast approval requires complete financial statements (profit and loss, balance sheet, tax returns for 2-3 years), business bank account statements, ownership documentation, property appraisals if collateral-based, and a clear business purpose statement. Audit-ready financials accelerate underwriting by reducing lender verification time. Missing documents force delays, so prepare everything upfront. Having a commercial loan documentation checklist ensures nothing is overlooked and speeds the application process significantly.

How can I speed up the commercial loan underwriting process?

Provide complete, accurate documentation immediately upon application. Respond to lender requests within 24 hours. Ensure financial statements are consistent and clearly show cash flow and debt service coverage ratio. Choose lenders with streamlined underwriting and direct funding capability rather than those using automated portals. Proactive communication, using clear templates and regular status updates, prevents misunderstandings that cause delays. Some lenders offer expedited underwriting for borrowers with strong credit scores and collateral.

What are the biggest pitfalls that delay commercial financing?

Incomplete documentation is the leading cause of delays. Inconsistent financial statements, missing tax returns, and unclear business purpose force re-submissions. Poor communication with lenders creates confusion and stalls approval. Underestimating collateral requirements or loan-to-value ratios causes rejection cycles. Waiting until the last moment to apply leaves no buffer for verification. Choosing lenders without direct funding power introduces additional delays through third-party brokers. Avoid these by preparing audit-ready financials, selecting lenders with transparent requirements, and maintaining clear, proactive communication throughout the process.

This article was written using GrandRanker