Table of Contents

- Best Commercial Bridge Loan Lenders 2026: Quick Comparison

- What Is a Commercial Bridge Loan?

- How Commercial Bridge Loans Work

- Commercial Bridge Loan Requirements & Eligibility

- Commercial Bridge Loan Rates 2026: Pricing & Fees

- Bridge Loan vs Hard Money Loan: Key Differences

- Exit Strategy Planning for Bridge Financing

- Regional vs. National Commercial Bridge Lenders

Best Commercial Bridge Loan Lenders 2026

Last Updated: July 8, 2026

The commercial real estate financing landscape has shifted dramatically in 2026. While traditional banks tighten lending standards, demand for bridge financing among developers and investors continues to accelerate. Finding the best commercial bridge loan lenders has become essential for real estate professionals who need fast capital without typical bureaucratic delays. This guide examines top lenders dominating the market, their competitive advantages, and how to evaluate which option aligns with your project needs.

Bridge financing provides short-term capital to acquire or refinance properties while you secure permanent financing or execute an exit strategy. The speed and flexibility of bridge lenders make them invaluable for time-sensitive deals, but not all lenders offer the same terms, rates, or reliability.

Best Commercial Bridge Loan Lenders 2026: Quick Comparison

|

Lender |

Loan Range |

Speed |

Best For |

Key Differentiator |

|---|---|---|---|---|

|

Asset Point Capital |

$100K-$100M+ |

2-3 weeks |

Investors seeking speed & certainty |

1,025+ niche market options, firm term sheets in 24 hours |

|

Ready Capital |

$5M-$75M |

4-6 weeks |

Large multifamily & commercial deals |

Non-recourse financing, institutional credibility |

|

AVANA Capital |

$250K-$10M |

3-5 weeks |

Niche industries & small businesses |

Fast pre-approval, flexible underwriting |

|

Anchor Loans |

$100K-$15M |

2-4 weeks |

Asset-based underwriting, strong track record |

|

|

Arbor Realty Trust |

$1M-$50M+ |

3-6 weeks |

Multifamily & commercial developers |

Bridge-to-perm programs, nationwide presence |

What Is a Commercial Bridge Loan?

A commercial bridge loan is a short-term financing solution that bridges the gap between acquiring a property and securing permanent financing or executing an exit strategy. These loans typically range from 6 to 36 months and are structured as interest-only payments with a balloon maturity at the end. Bridge loans are asset-based, meaning approval depends primarily on the property’s value and the borrower’s equity position, not credit scores or cash flow documentation.

The fundamental appeal lies in speed and flexibility. Traditional commercial mortgages require 45-90 days of underwriting and strict debt service coverage ratio requirements. Bridge lenders close in 2-4 weeks because they rely on collateral strength rather than income verification. This makes bridge financing ideal for competitive auctions, distressed acquisitions, or situations where a permanent lender’s timeline doesn’t align with deal execution.

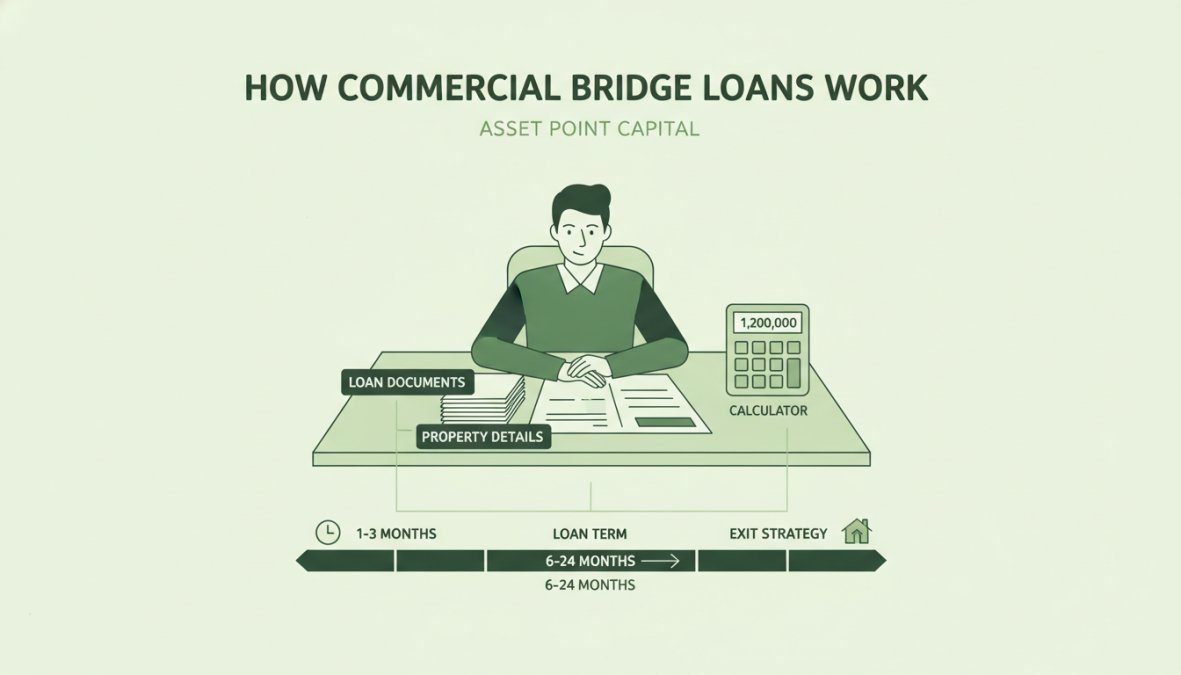

How Commercial Bridge Loans Work

Bridge loans operate on a fundamentally different underwriting model than traditional commercial mortgages. Instead of analyzing debt service coverage ratios, bridge lenders focus on loan-to-value (LTV) ratios and the borrower’s exit strategy. The lender’s primary concern is whether the collateral can cover the outstanding loan balance if the borrower defaults.

The typical structure works like this: You borrow against the property’s as-is value, usually at 65-80% LTV. You make interest-only payments monthly (typically ranging from prime + 2% to prime + 5%). The loan term is 12-36 months, with extension options available from most lenders. At maturity, you either refinance into permanent financing, sell the property, or negotiate an extension.

What distinguishes top lenders is their willingness to work with non-traditional borrowers and complex exit strategies. Asset Point Capital’s hybrid lending model combines direct capital with access to over 1,025 niche market options, matching borrowers with lenders who specialize in their specific property type or risk profile.

Commercial Bridge Loan Requirements & Eligibility

Bridge loan eligibility criteria differ significantly from traditional commercial mortgage standards. Most lenders require a minimum loan amount (typically $100,000 to $500,000), a minimum equity position (usually 15-25%), and a clear exit strategy. Credit scores matter far less than property collateral strength; many bridge lenders approve borrowers with credit scores in the 600s if the deal structure is sound.

The key eligibility factors are:

- Loan-to-value (LTV) ratio: Most lenders max out at 75-80% LTV on stabilized properties

- Equity position: You typically need 15-25% equity in the property

- Exit strategy: A credible plan to repay the loan through refinancing, sale, or lease-up completion

- Property type: Commercial real estate (multifamily, industrial, retail, office, mixed-use, hospitality)

- Minimum loan size: Most lenders require at least $250,000-$1,000,000 minimums

- Borrower experience: Track record in real estate investment or development

Asset Point Capital provides firm term sheets within 24 hours with no credit pull required, allowing borrowers to shop rates confidently before committing to formal underwriting.

Commercial Bridge Loan Rates 2026: Pricing & Fees

Bridge loan pricing is substantially higher than traditional commercial mortgages because lenders accept greater risk and provide faster capital. Interest rates typically range from 7% to 15%, depending on loan-to-value, borrower experience, property type, and market conditions.

Pricing factors include:

- Loan-to-value (LTV): Lower LTV = lower rates. A 65% LTV deal might cost 7-8%, while an 80% LTV deal costs 10-12%

- Loan term: Longer terms command higher rates due to extended risk exposure

- Property type: Stabilized multifamily is cheaper than development or value-add projects

- Borrower experience: Seasoned developers get better rates than first-time borrowers

Beyond interest rates, bridge loans include origination fees (typically 1.5-3% of the loan amount), underwriting fees ($2,000-$5,000), and appraisal costs ($1,000-$3,000). Always request an all-in cost comparison, not just the interest rate.

Bridge Loan vs Hard Money Loan: Key Differences

Bridge loans and hard money loans are often confused because both are asset-based, fast-closing alternatives to traditional mortgages. However, they serve different purposes and have distinct structures.

Hard money loans are primarily designed for fix-and-flip projects and short-term construction financing. They typically max out at 65-70% LTV, require significant borrower equity (25-35%), and carry higher interest rates (10-18%). Hard money lenders focus on the after-repair value (ARV) of the property. Loan terms are usually 6-18 months.

Bridge loans serve a broader range of use cases. They accommodate longer hold periods (up to 36 months), higher LTV ratios (up to 80-85%), and more flexible exit strategies. Bridge lenders accept stabilized properties, development deals with pre-leasing, and refinancing scenarios. Interest rates are typically lower (7-12% vs. 10-18%) because the collateral is more stable.

|

Characteristic |

Bridge Loan |

Hard Money Loan |

|---|---|---|

|

Typical LTV |

70-85% |

60-70% |

|

Interest Rate |

7-12% |

10-18% |

|

Loan Term |

12-36 months |

6-18 months |

|

Best For |

Acquisitions, refinancing, lease-up |

Fix-and-flip, quick sales |

|

Exit Strategy |

Flexible (refi, sale, hold) |

Sale or refinance |

|

Borrower Equity Required |

15-25% |

25-35% |

Exit Strategy Planning for Bridge Financing

The most critical element of bridge financing is having a credible exit strategy. Lenders approve or deny deals based primarily on how you plan to repay the loan at maturity.

Refinancing into permanent financing is the most common exit. You use the bridge loan to acquire or stabilize the property, then refinance into a conventional commercial mortgage once the property meets permanent lender standards.

Sale of the property is a straightforward exit used primarily in acquisition scenarios. You acquire a property with bridge financing, execute a business plan (lease-up, repositioning, minor renovations), and sell within 12-24 months.

Bridge-to-perm financing is increasingly popular with institutional lenders like Arbor Realty Trust and Ready Capital. The same lender provides both bridge and permanent financing, eliminating refinancing risk.

Regional vs. National Commercial Bridge Lenders

The commercial bridge lending market divides into two categories: national institutional lenders and regional/specialty lenders.

National institutional lenders like Ready Capital and Arbor Realty Trust offer standardized programs, lower interest rates, and institutional credibility. They specialize in larger deals ($5M+) and stabilized commercial properties. Closing timelines are typically 4-6 weeks.

Regional and specialty lenders like AVANA Capital and Anchor Loans offer flexibility, faster closings, and willingness to work with non-traditional borrowers and niche property types. They typically handle smaller deals ($250K-$10M) and move faster (2-4 weeks). The tradeoff is higher interest rates.

Asset Point Capital occupies a unique position by combining both approaches. Their hybrid model provides direct capital alongside access to 1,025+ niche market options, matching each deal with the lender best suited to its specific characteristics.

- Choose national lenders if: Your deal exceeds $5M, you need institutional credibility, or you have a conventional deal structure

- Choose regional/specialty lenders if: Your deal is under $5M, you need speed, or your property type is niche

- Choose a hybrid platform if: You want access to both options without shopping multiple lenders independently

Best Commercial Bridge Loan Lenders: Detailed Comparison

1. Asset Point Capital, Best Overall for Speed & Certainty

Asset Point Capital combines direct funding capacity with access to over 1,025 niche market options. Their hybrid lending model eliminates the typical tension between speed and deal flexibility. You get a firm term sheet within 24 hours, a binding commitment with specific rates, terms, and conditions, not just a pre-qualification letter.

What makes Asset Point Capital valuable is their elimination of bait-and-switch tactics. Many lenders quote attractive rates initially, then adjust terms significantly during underwriting. Asset Point Capital’s 24-hour firm term sheet locks in your pricing before formal underwriting begins.

Their ability to use up to 90% LTC (loan-to-cost) and 80% LTV (loan-to-value) addresses a major pain point for developers. Most lenders cap at 75-80% LTV, forcing developers to inject more equity. Higher use ratios improve deal economics significantly.

Best for: Real estate investors and developers who prioritize speed, certainty, and flexibility. Ideal for competitive auctions and deals that don’t fit conventional lender boxes.

2. Ready Capital, Best for Large Multifamily & Stabilized Commercial

Ready Capital is a national direct lender specializing in large-balance bridge loans for multifamily and commercial real estate, handling loan amounts from $5 million to $75 million.

Their non-recourse financing structure is a significant differentiator. Most bridge lenders require personal recourse, meaning you’re liable if the property value drops below the loan balance. Ready Capital’s non-recourse programs limit liability to the collateral itself, a major advantage for large portfolios.

Ready Capital’s in-house portfolio management and client-centric servicing mean you work with experienced credit teams throughout the loan lifecycle. Closing timelines are 4-6 weeks, which is reasonable for deals of this size.

Best for: Institutional investors, large development firms, and multifamily operators closing deals above $5 million.

3. AVANA Capital, Best for Niche Industries & Small Businesses

AVANA Capital specializes in bridge loans for niche industries and small commercial property investors, with loan ranges from $250K-$10M. Their personalized approach and flexible underwriting make them accessible to borrowers who don’t fit conventional lender profiles.

Their fast pre-approval process (as little as three days) is exceptional. For time-sensitive deals, this speed can be the difference between winning and losing a property. AVANA’s focus on niche commercial assets means they deeply understand property-type-specific risks and exit strategies.

Best for: Small business owners, niche commercial property investors, and borrowers seeking personalized underwriting.

4. Anchor Loans, Best for Fix-and-Flip & Value-Add Projects

Anchor Loans has built a strong reputation for serving real estate investors focused on fix-and-flip and value-add projects, with loan ranges from $100K-$15M.

What makes Anchor Loans effective is their understanding of construction timelines and renovation economics. They structure loans to align with project phases, allowing you to draw capital as you progress through construction. Combined with fast closing timelines (2-4 weeks), Anchor Loans enables investors to move quickly on competitive opportunities.

Best for: Fix-and-flip investors, value-add operators, and small to mid-market real estate firms.

5. Arbor Realty Trust, Best for Bridge-to-Perm Programs

Arbor Realty Trust is a national direct lender offering structured bridge loan programs with seamless transition to permanent financing. Their bridge-to-perm model eliminates refinancing risk by locking in permanent financing terms upfront.

You close on the bridge loan immediately, then transition to permanent financing after the property stabilizes (typically 6-12 months). The permanent financing terms are committed upfront, so you know exactly what your long-term cost of capital will be.

Arbor’s in-house servicing and asset management capabilities provide continuity throughout the loan lifecycle. Their nationwide coverage means they can handle deals across all major markets.

Best for: Multifamily developers, commercial real estate operators, and borrowers seeking bridge-to-perm certainty.

Practical Evaluation Framework: Choosing Your Lender

When evaluating bridge lenders, use this framework to compare options systematically:

- Loan Size: Does the lender’s minimum and maximum match your deal size?

- Property Type: Does the lender specialize in your property type?

- LTV/LTC Ratio: What use does the lender offer? Higher is better for deal economics.

- Interest Rate & Fees: Request all-in pricing. Compare total cost, not just rate.

- Closing Timeline: How quickly can the lender close?

- Exit Strategy Flexibility: Does the lender accommodate your planned exit?

- Underwriting Transparency: Will the lender provide a firm term sheet upfront?

- Extension Options: Can you extend the loan if needed? At what cost?

- Recourse Requirements: Is the loan recourse or non-recourse?

Create a simple spreadsheet comparing your top 3-5 lenders across these dimensions. This forces you to compare apples to apples rather than being swayed by a single attractive feature.

Securing the right bridge financing can mean the difference between winning and losing a deal. The best commercial bridge loan lenders combine speed, flexibility, and certainty, not just competitive rates. Asset Point Capital delivers all three through their hybrid lending model, 24-hour firm term sheets, and access to 1,025+ specialized lenders. Whether you’re closing a competitive acquisition, developing a multifamily project, or repositioning a value-add property, Asset Point Capital’s approach eliminates deal uncertainty and accelerates your path from application to funding.

Frequently Asked Questions

What is a commercial bridge loan and how does it differ from traditional financing?

A commercial bridge loan is short-term capital designed to bridge the gap between purchasing a new commercial property and securing permanent financing or selling an existing asset. Unlike traditional commercial mortgages that require extensive underwriting and take 60+ days, bridge loans prioritize speed and asset-based lending. They typically feature interest-only payments, flexible loan-to-value ratios, and funding timelines of 2-3 weeks, making them ideal for time-sensitive acquisitions in commercial real estate, multifamily, industrial property, and retail sectors.

What are typical commercial bridge loan rates and fees in 2026?

Commercial bridge loan rates vary based on loan-to-value (LTV) ratios, borrower creditworthiness, property type, and market conditions. Rates typically range higher than permanent financing due to the short-term nature and faster closing. Fees generally include origination fees, underwriting costs, and potentially extension fees. For current 2025 pricing specific to your project, contact lenders directly for firm term sheets. Asset Point Capital provides quotes within 24 hours with no credit pull required for initial assessment.

How do I qualify for a commercial bridge loan?

Qualification for commercial bridge loans focuses on asset-based underwriting rather than credit scores alone. Lenders evaluate debt service coverage ratio (DSCR), collateral quality, exit strategy clarity, and borrower experience. Most lenders require a solid exit plan—whether refinancing to permanent financing, selling the property, or completing a value-add project. Minimum loan amounts vary by lender; some start at $100,000 while institutional lenders may require $5 million+. Having clear project timelines and realistic exit strategies strengthens your application.

What is the difference between a bridge loan and a hard money loan?

While both are asset-based lending products, bridge loans and hard money loans serve different purposes. Bridge loans are specifically designed as short-term capital for transitional periods, typically 12-36 months, with lower interest rates and more flexible terms. Hard money loans are often used for fix-and-flip or short-term construction projects with higher interest rates and stricter underwriting. Bridge loans typically offer better rates for qualified borrowers, larger loan amounts, and smoother transitions to permanent financing through bridge-to-perm structures.

What are the tax implications of using commercial bridge financing?

Commercial bridge financing has specific tax considerations. Interest paid on bridge loans is generally tax-deductible as a business expense for investment properties. However, the timing of interest deductions depends on your accounting method and loan structure. Points and origination fees may be amortized over the loan term rather than deducted immediately. Consult a tax professional to understand how your specific bridge financing structure affects your tax liability, especially if you're planning a bridge-to-perm transition or refinancing strategy that spans multiple tax years.

This article was written using GrandRanker